As 2024 comes to a close, it’s the perfect time for business owners to engage in year-end tax planning. Proper planning not only ensures compliance but also allows you to maximize deductions and credits, ultimately saving your business money. With the tax landscape constantly changing, now is the time to strategize and take advantage of every opportunity available.

Let’s explore some effective year-end tax planning strategies to help your business save before 2025.

1. Review Your Business Structure

The structure of your business—whether it’s a sole proprietorship, partnership, LLC, or corporation—has significant tax implications. As your business grows, it might be beneficial to reevaluate your structure to ensure you’re taking advantage of the most favorable tax treatment.

- C Corporations vs. S Corporations: Consider whether an S Corporation might save you money on self-employment taxes or if a C Corporation would be better for retaining earnings.

- Partnerships: If you operate as a partnership, ensure you’re aware of how partnership distributions impact your taxable income. Consider a limited partnership with your spouse to lower self-employment taxes.

Consulting with a tax professional can provide insights into the best structure for your growing business.

2. Maximize Retirement Contributions

Contributing to retirement plans is a dual benefit: it helps you save for the future while reducing your taxable income today.

- 401(k) Plans: If you have a 401(k) plan, maximize your contributions. For 2024, the contribution limit is $22,500, or $30,000 if you’re 50 or older.

- SEP IRAs: If you’re self-employed or a small business owner, consider a Simplified Employee Pension (SEP) IRA, which allows for larger contributions compared to traditional IRAs.

- SIMPLE IRAs: Allow owners and employees to contribute pre-tax and the business can

- match employee contributions for additional tax savings.

These contributions lower your taxable income, thus reducing your overall tax liability for the year.

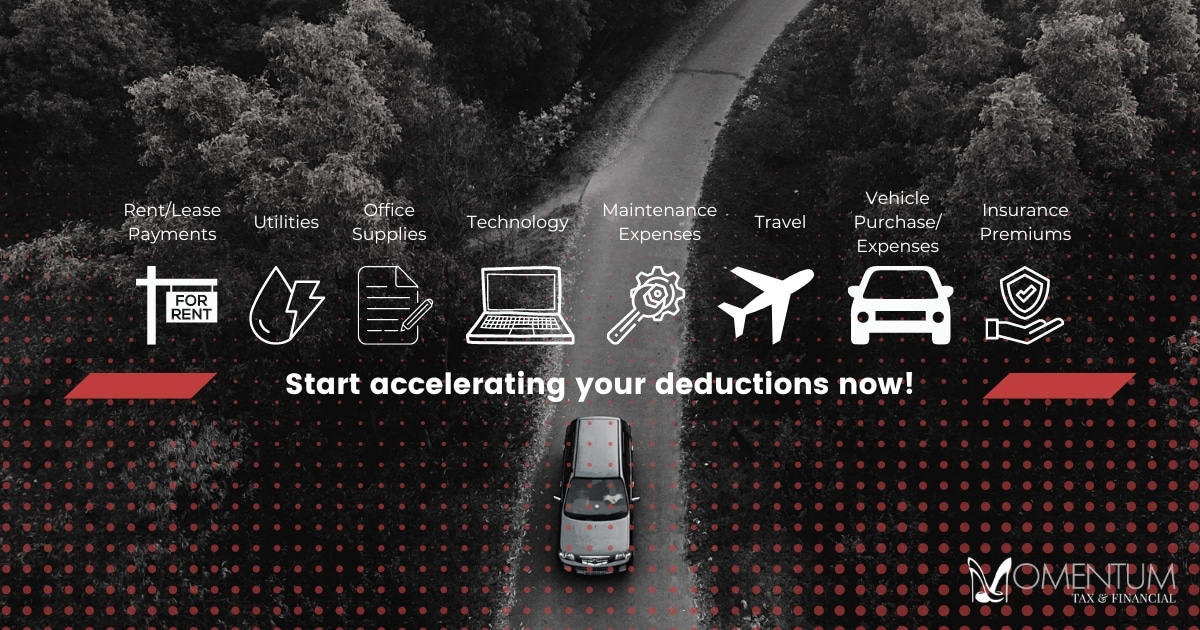

3. Accelerate Deductions

One effective strategy for year-end tax planning is to accelerate deductions. This means you should look for ways to take deductions in 2024 rather than deferring them to 2025.

- Prepay Expenses: If possible, prepay any expenses for 2025—such as rent, utilities, or supplies—before December 31. This allows you to deduct them this year.

- Asset Purchases: Consider making large purchases or investments in equipment or technology that qualify for Section 179 expensing or bonus depreciation. These deductions can significantly reduce your taxable income.

4. Defer Income

Deferring income can be a smart move if you anticipate being in a lower tax bracket next year.

- Shift Revenue Recognition: If your business uses the cash method of accounting, consider delaying invoicing clients until January 2025. This keeps the income out of your 2024 taxable income.

- Year-End Bonuses: If you plan to give year-end bonuses, consider delaying them until January.

This strategy can lower your current year’s taxable income and provide more flexibility in managing your cash flow.

5. Utilize Tax Credits

Tax credits directly reduce your tax liability and can offer substantial savings. Familiarize yourself with available credits that may apply to your business:

- Employee Retention Credit: If your business retained employees during challenging times, you may be eligible for this credit.

- Research and Development Credit: If your business invests in innovation, this credit can help offset costs.

Make sure to conduct a thorough review to ensure you’re claiming all the credits you qualify for.

6. Take Advantage of Health Savings Accounts (HSAs)

If your business offers high-deductible health plans, consider establishing Health Savings Accounts (HSAs) for you and your employees. Contributions to HSAs are tax-deductible and can be used for qualified medical expenses.

- Contribution Limits: For 2024, the contribution limit is $3,850 for individual coverage and $7,750 for family coverage, with an additional $1,000 for individuals aged 55 and over.

- Tax-Free Withdrawals: Funds can be withdrawn tax-free for medical expenses, making HSAs a valuable tool for managing health care costs.

7. Conduct a Year-End Inventory Assessment

For businesses that maintain inventory, a year-end assessment is crucial.

- Inventory Valuation: Determine the value of your inventory using an appropriate accounting method (FIFO, LIFO, or weighted average).

- Write Off Obsolete Inventory: If you have outdated or unsellable inventory, consider writing it off before the year ends. This can lead to a significant tax deduction.

This assessment helps you manage cash flow better and allows for more informed business decisions in the coming year.

8. Evaluate Your Accounts Receivable

An often-overlooked area for tax planning is accounts receivable.

- Collect Outstanding Invoices: Make an effort to collect any outstanding invoices before the year ends. This not only helps improve cash flow but also ensures you recognize that income in 2024.

- Write Off Bad Debts: If you have accounts receivable that are unlikely to be collected, consider writing them off as bad debts. This deduction can lower your taxable income.

9. Stay Informed on Tax Law Changes

Tax laws are ever-evolving, and staying informed is crucial for effective tax planning.

- Legislation Updates: Keep an eye on any changes to tax legislation that may impact your business. For example, changes in rates, deductions, and credits could affect your overall tax strategy.

- Engage a Tax Professional: Collaborate with a tax advisor or CPA who can provide insights tailored to your specific situation. They can help you navigate the complexities of tax regulations and make informed decisions.

Tax Planning Starts Now for a Successful 2025

As the year winds down, proactive tax planning can lead to significant savings for your business. By implementing these strategies, you can position your business for financial success as you enter 2025. Whether it’s maximizing deductions, deferring income, or taking advantage of credits, every action you take now can have lasting benefits.

At Momentum Tax, we’re here to guide you through these strategies and ensure you’re making the most of your year-end tax planning.

Reach out to us today to discuss how we can help you save money and optimize your tax situation before the clock strikes midnight on December 31!